It’s the new buzzword. PropTech is coming and is about to disrupt the real estate industry.

It’s the new buzzword. PropTech is coming and is about to disrupt the real estate industry.

But what exactly is PropTech? Why has it been such a news item lately? What does PropTech mean for real estate professionals? Who will be affected? What are the issues at stake?

Between automatization and uberisation, PropTech is both threatening and promising. Here is what you need to know.

Two years ago no one talked about PropTech. Yet, many real estate startups were already gearing up to disrupt the industry. A few of them, such as Zillow in the US, have been doing it for a long time; others are still trying and will keep on trying. But today the landscape has changed. PropTech is the talk of the town. The market moves at a faster pace. First off, let’s define this trend.

What Is Proptech?

There are many ways to define PropTech. Here is one of the most widely shared views, by James Dearsley.

Proptech is one small part of a wider digital transformation in the property industry. It considers both the technological and mentality change of the real estate industry, and its consumers to our attitudes, movements and transactions involving both buildings and cities.

It is a somewhat vague concept, but one that clearly affects a wide spectrum of the “real estate” sector. Indeed, here we are talking about the commercial side of the industry as well as the construction side, and even about the buildings and cities of the future. No wonder entrepreneurs, investors, and journalists are so eager to claim ownership of the trend. Many have attempted to provide a plain language definition of what it encompasses. The best and most straightforward definition is as follows:

It’s a collective term used to define startups offering technologically innovative products or new business models for the real estate markets.

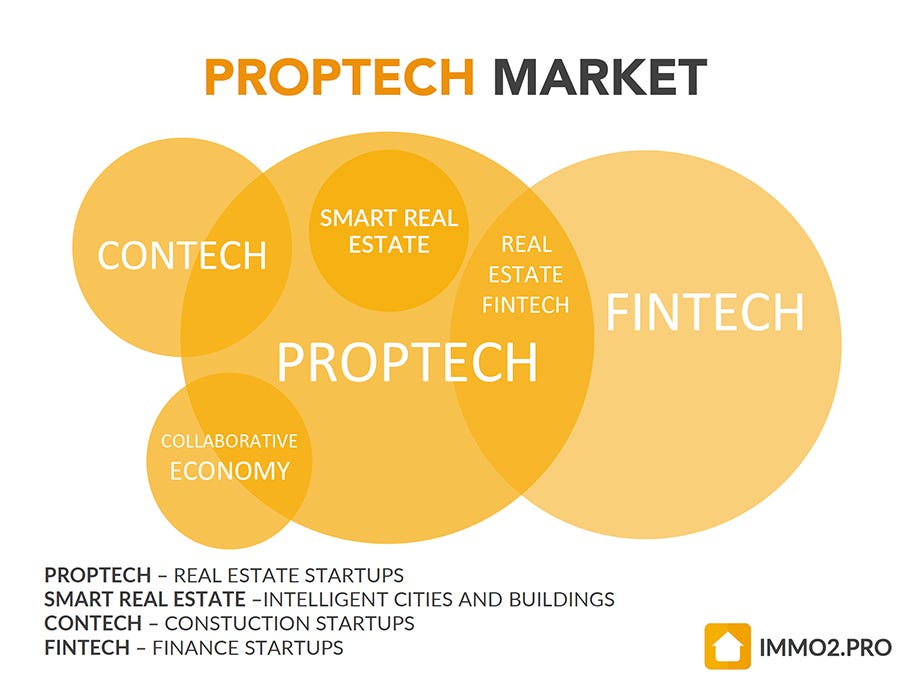

In short, it stands for all the companies that are taking on the real estate industry to make it better, spurred by an ever-changing digital landscape and new consumption patterns. It is still a new trend, and its scope will surely evolve as time goes by. Today, several verticals emerge within PropTech: the real estate market per se (PropTech), smart cities and buildings, the sharing economy, the home building industry (ConTech) and finance (FinTech). Both ConTech and FinTech have very close ties with the real estate industry. To get a clearer picture, take a look at this diagram:

Of course, none of this is new. But with many sectors now being “uberised”, real estate has become a prized target, especially for investors.

The Rise Of Venture Capital Funding

Investment money allows to quickly bring a new service to market and topple long-standing barriers. Fundraising by startups operating in the real estate sector is by no means new. But since 2014 the sector has been experiencing strong growth, and is now tracked officially. One might think that global business leaders got wind that something was up in the sector and that it was high time they caught up so they could be the ones reaping the rewards. Take a look at how fast investments have grown over the last few years.

Also worth noting is the fact that the first PropTech startup valued at over $1 billion was founded in 2016. And three more followed in its footsteps the same year.

The Legend Of Unicorns

A unicorn is a company worth over $1 billion. In the real estate industry, Compass was the first one to reach that milestone; Homelink and SMS Assist quickly followed. And then of course, Opendoor. What’s interesting here, is that the trend is not solely restricted to the US and Silicon Valley because Homelink is a Chinese real estate portal. Thus PropTech is a truly global phenomenon. Besides, each one of these 4 startups is fundamentally different in nature and scope. The first one is a network of real estate brokers, the second one a portal, the third one a property management tool, and the last one has developed an algorithm for buying and selling homes online. Undeniably, the 4 PropTech unicorns cover a wide spectrum. And with $6.4 billion raised over the past 4 years among more than 800 registered real estate startups, many of the traditional real estate professions are being targeted by the newcomers.

Which Real Estate Professions Is Proptech Going After?

So it’s pretty clear at this point that all sectors of the real estate industry are being threatened by the rise of PropTech. The Guarantors or SMS Assist are making inroads in rental property management; TenX, OpenDoor, or Purplebricks, in real estate sales; VTS in commercial real estate; Habiteo in real estate development, etc. These are but a few examples but there are dozens of startups in each profession. No sector is spared.

However, there is a marked difference between new and existing construction. Indeed, in existing real estate, numerous startups are lined up to eliminate and replace industry professionals. In new construction on the other hand, startups mostly operate as middlemen or as suppliers of hi-tech tools for developers. For the time being, that is.

Furthermore, new trends are emerging across all sectors of the real estate industry: co-working is disrupting the office space sector, co-living is offering new alternatives in residential real estate, crowdfunding is reshaping new construction and real estate investing, and home swapping is growing increasingly popular for seasonal rentals. Many new professions such as drone pilots, virtual home staging specialists or data aggregators have also appeared alongside traditional real estate industry jobs. And you can bet that every five minutes new ideas are being floated that will reinvent all or part of the real estate industry.

These dynamics are prompting entrepreneurs and innovators to reflect on various aspects of the industry and to create startups addressing highly specific needs.

What Are The Different Categories Of Startups?

Analyzing the PropTech sector is both a simple and complex task when you consider the many ways in which startups are using technological innovations to disrupt the real estate industry. Without claiming to be exhaustive, let’s mention for example the use of artificial intelligence by room.ai, beacons by Smart Service Connect, smart home viewing booking tools by Front Door, blockchain technology by Ubitquity, virtual reality by Matterport, augmented reality by Datrix, or data visualization by Create.io. Others are using connected objects, 3D printing, mobility technology, big data, etc.

There are thousand ways in which startups are pushing the boundaries of innovation in the real estate industry. Most companies actually combine several areas of expertise. Consider Opendoor. The startup purchases property online directly from homeowners and at a price set by a proprietary algorithm driven by big data. After calling in a specialized team to renovate and upgrade the property, it then puts it back on the market, using connected locks and cameras to enable self-guided visits from prospective homebuyers. Here several know-hows are on display, such as mobility technology, big data, connected objects, digitization, etc.

Why these startups have a competitive advantage is because of their ability to bring innovation into each step of the process and radically rethink existing systems. And it’s indeed worth pointing out: PropTech startups come in with a new vision and a desire for reinvention; starting from scratch, they want to rewrite the book on tomorrow’s real estate industry. They might address one highly specific aspect of the industry such as BIM management and coordination between the many actors of the construction business, or they might take on the entire business model, such as is the case with rental property management or transactions for existing residential properties.

Most startups thus fall into one of two main categories:

- Startups offering support for real estate professionals, such as tools to enhance their services or their productivity;

- Startups proposing to replace real estate professionals.

Therefore, the stakes are high for real estate professionals.

Proptech: What’s At Stake For Real Estate Professionals?

First of all, the fact that someone came up with a name for a new industry implies that the trend is real and clearly defined. It also means that some people find it valuable and by “people” meaning by “investors”. No wonder funds such as Fifth Wall Ventures — which raised $212 million — were set up to invest in PropTech. You can bet that sooner of later a number of promising startups are going to come out of the woods and start fighting for a piece of the real estate cake.

Remember how the music industry turned a deaf ear to its challengers? Overly self-confident, it was unable to address the changes affecting music consumption. Today Spotify, Deezer or YouTube control music distribution across the globe. Same story with Kodak and digital photography. The risk is very real and potentially affects many sectors.

There is an interesting article on FinTech, which is more or less the same thing as PropTech but applied to the financial sector. Its assessment was that banks are not worried at all about newcomers. They’re still making money, and quite a lot of it. Back in the day, Universal, Kodak, and the taxi industry too had quite a bit of cash at hand to fight the new kids on the block. But the problem is more deeply rooted. Business models are being reevaluated, consumers’ needs are evolving. Newcomers are able to dig deep and analyze these changes to offer better solutions and improved customer experiences. Ultimately, they’ll come out ahead.

For example, Opendoor is replacing real estate professionals for clients in Dallas, Phoenix, and Las Vegas who want to sell their property fast. In Britain, Alex Gosling, CEO of HouseSimple, says that online real estate brokers have captured 5% of the market and estimates that they might reach 15 to 20% by 2020.

One might think that real estate developers are more immune to this trend because they control production and therefore can’t easily fall victim to disintermediation. Today indeed it’s hard to imagine that a company might be able to use big data to locate building land, apply blockchain technology to streamline the purchasing process, print 3D models of homes and buildings, and use virtual reality to offer guided visits to sell these properties on the Internet. But in 10 years from now, this might be a reality.

Technology is what helps keep the real estate industry on its toes. Increasingly, new actors are flooding the market, offering tools and solutions for real estate professionals, or harboring the ambition to become the Uber of real estate.

How Should Real Esate Professionals Address The Rise Of Proptech? What Solutions Can Be Offered?

All in all, it’s pretty straightforward. It begins with the realization that change is real and inevitable and will happen with or without real estate professionals. There’s no reason to fear change though, all you need to do is embrace it and keep working with your clients — current and future. Here are a few helpful tips to guide you along the way:

- Keep Up With Industry News: Read specialized websites regularly. The more informed you are, the better your ability to anticipate changes in the market and meet the needs of your clients wherever they happen to be.

- Invest: Invest in equipment and marketing tools so you remain up to date as far as technology is concerned.

- Experiment: You’re in luck. You have existing clients and you are out in the field everyday. Test new tactics and find out which ones are successful.

- Innovate: Each week, spend a minimum of 2 hours thinking about how you might improve the way you work or client satisfaction. This will ensure you remain competitive in the marketplace, no matter what happens because of PropTech.

- Work On Your Added Value: This is key. Try answering the question: “Why do clients come and see me?” Once you’ve formulated the answers, make sure you deliver on them consistently so clients won’t want to go elsewhere.

- Keep In Touch With Your Clients: Go the extra mile. Ask your clients for feedback. Would they recommend you to their friends? Why not? The best way to improve client satisfaction is by serving your clients’ needs.

- Keep Up With The Younger Generations: Remain open-minded and mindful of their changing consumption patterns. Younger generations are tomorrow’s clients

Do Not Forget: The Key Is To Keep Up To Date And Avoid Denial

Today as a real estate professional with a portfolio of clients, you are in the best position to know and anticipate their needs. Innovation and technology won’t succeed if they don’t fulfill clients’ needs. So if your clients are satisfied, technology and innovation are not necessary. It’s up to you to address your clients’ needs. Technology is only a means to an end.

Source: Medium