Any conversation about taxes is enough to make eyelids heavy. Watching paint dry can seem preferable to discussing the topic.

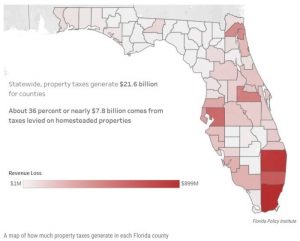

Florida’s House of Representatives just voted in favor of the state’s plan to eliminate property taxes despite not addressing how to replace the revenue that the taxes currently generate. The Senate has yet to vote on the measure, and if it passes, it will appear on the general election ballot this November. That earlier analysis raised the principle that “there’s no such thing as a free lunch” and highlighted the absence of any plan to replace the lost revenue needed to fund local government services such as police and fire protection, schools, and other essential functions. It bears repeating that there is literally no replacement funding plan despite the House’s favorable vote.

The proposal represents a direct threat to the quality of life enjoyed by both current and future Florida residents. While supporters see the elimination of property taxes as a deserved gift—a free lunch—even modest critical thinking reveals significant risks to housing affordability, market stability, and the reliability of basic public services, all of which play a role in property valuation. Further reflection on the issue prompts a deeper examination of property taxes and how they compare to other government revenue sources.

Taxes Can Be Damaging When They Change Behavior

Tax policymakers at the city, state, and federal levels often overlook how individuals alter their behavior to avoid taxation. This tendency continues to be ignored. If work is taxed, people tend to work less. If sales are taxed, there tend to be fewer sales. The same principle applies broadly across taxation. The ideal—or perhaps least harmful—tax targets assets with a fixed supply, such as land, because they cannot disappear or relocate in response to taxation. This principle forms one of the primary criticisms of New York City’s pied-à-terre tax.

Why Land Is the Most Efficient Type Of Tax

Land is inelastic in supply. As the saying goes, “they’re not making it anymore.” Because land cannot be created or removed, taxing it does not reduce its supply. Even conventional property taxes, which apply to both land and improvements, still derive much of their tax base from land itself, resulting in relatively little economic distortion to labor, materials, or business activity.

Because land is immovable and easily observable—with perhaps the exception of Florida swamp land, as old jokes suggest—it is much harder to evade taxation through legal maneuvering or profit shifting than income or corporate taxes. As a result, municipalities can raise revenue with lower tax rates and reduced administrative costs associated with enforcement.

Property taxes remain the dominant source of revenue for local governments and school districts because they are generally more stable year to year than income or sales tax revenues. This stability reduces the frequency of tax increases or service reductions needed to balance budgets.

Another major advantage is the direct connection between those who pay property taxes and those who benefit from the resulting services. Taxpayers can often observe local investments reflected in higher property values, partially offsetting the burden of taxation. Because property taxes are highly visible and billed separately, voters can more easily connect tax levels to service quality, helping to constrain government spending without creating the economic distortions associated with income or sales taxes.

When evaluating communities, the relationship between school spending and property values often becomes apparent. Communities that spend more per student frequently exhibit higher property values, suggesting stronger educational systems and greater demand from homebuyers.

The Problem With Property Taxes

Property tax systems are not without flaws. Assessment practices can create regressive and inequitable outcomes, particularly in places such as New York City, where a convoluted system can effectively lock in benefits for longtime property owners and discourage turnover. New York State currently has the third-highest property tax burden in the country, while Florida ranks 28th.

Taxing improvements along with land can also discourage denser, higher-value development. This reality strengthens the argument for a land-value-only tax or a system that taxes land more heavily than structures. Flat property taxes can be particularly burdensome for homeowners and renters who are asset-rich but cash-poor. This helps explain the popularity of circuit-breaker programs and homestead exemptions, such as those used in Florida.

Why There Are No “No Property Tax” States

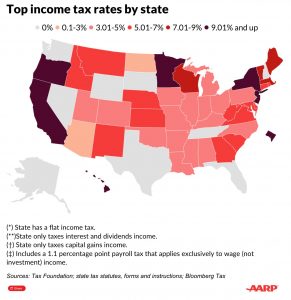

As of 2025–2026, nine states impose no broad-based personal income tax, yet every state in the nation still levies some form of property tax, typically at the local level.

All 50 states and the District of Columbia rely on property taxes somewhere within their municipal finance systems, even when state governments themselves do not impose statewide property taxes. Property taxation serves primarily as a local revenue source for cities, counties, school districts, and special districts, helping fund K–12 education and other local services.

Some states maintain very low effective property tax rates—Hawaii, Alabama, and Wyoming among them—but none have reduced those rates to zero. Property taxes are deeply embedded within the nation’s fiscal structure, particularly for school funding and municipal bond financing. Eliminating them entirely would require politically significant shifts toward higher sales taxes, higher income taxes, or state-controlled school finance systems.

Some states maintain very low effective property tax rates—Hawaii, Alabama, and Wyoming among them—but none have reduced those rates to zero. Property taxes are deeply embedded within the nation’s fiscal structure, particularly for school funding and municipal bond financing. Eliminating them entirely would require politically significant shifts toward higher sales taxes, higher income taxes, or state-controlled school finance systems.

In practice, some states without income taxes rely more heavily on property taxes to compensate for the absence of income tax revenue. Texas is a frequently cited example, with relatively high effective property tax rates despite having no state income tax.

Final Thoughts

Eliminating property taxes would do more than create a budget shortfall. It would transfer power away from local governments and weaken the direct relationship between taxation, public services, and home values.

By removing local property tax bases while simultaneously controlling how remaining revenues are distributed, the proposed constitutional amendment would effectively force counties and municipalities to depend on Tallahassee for permission and funding to maintain schools, public safety, infrastructure, and community amenities.

This type of centralization contrasts sharply with Florida’s reputation as a small-government state. Instead, it would create a highly centralized, state-directed tax-and-spend system in which political decisions made in Tallahassee determine winners and losers rather than local fiscal priorities and community needs.

Supporters are pursuing a constitutional amendment because Florida’s property tax structure is embedded in the state constitution, making constitutional change the most effective way to implement a broad and durable transformation.

No state has taken this step before, and there are compelling reasons why. Such a change would make housing markets less predictable by forcing buyers to consider state-level political decisions rather than local conditions. Replacing property taxes with more volatile revenue sources, such as income or sales taxes, would also make local government funding less stable, increasing uncertainty and potentially placing downward pressure on property values.

Over time, this could make Florida less attractive to the steady middle- and upper-middle-income households that have played a significant role in driving the state’s recent real estate success.

Ultimately, the power shift toward Tallahassee embodied in this proposal could undermine Florida’s positive real estate growth story if voters approve it this fall.

Source: The Real Deal